Apple will be revealing the details of its fourth-quarter and full-year earnings for 2024 with its financial results release and conference call on October 31. Here's what to expect from Apple, as well as the expectations of analysts watching the company.

Apple's quarterly earnings report will be released on Halloween, ahead of its investor and analyst conference call at 5 PM Eastern time.

While the call will feature CEO Tim Cook and CFO Luca Maestri discussing the financial results with a bit more color, it will be an unusual event. Maestri is stepping down as CFO at the end of 2024, making it his last investor call before Kevan Parekh takes the role.

Even after this week of Mac releases, AppleInsider will be listening to the conference call and reporting the financial results in full.

Product launches

While the fourth quarter typically deals with the financial for a three month period until the end of September, the products that affect it can be released a lot earlier. Releases late in the period will matter more for the next financial year, when more time has passed for sales.

For example, the iPhone 16 generation release on September 20, as well as USB-C AirPods Max, AirPods, the Apple Watch Series 10, and the Apple Watch Ultra 2 in a new black colorway black, won't make that much of a dent in the finances. However, with high holiday quarter sales on the horizon, they will be more important in the Q1 2025 results than in Q4 2024.

The Q3 2024 releases will have enjoyed over an entire quarter of sales, making them more impactful. This means the iPad Pro update to M4, the iPad Air with M2, and the Apple Pencil Pro.

The quarter was also absent any Mac Mac launches. However, any upcoming Mac updates will only affect the Q1 2025 results.

One year ago - Q4 2023

The yardstick that the Q4 2024 results will be based on, the Q4 2023 financials will help give investors a sign of where Apple is headed.

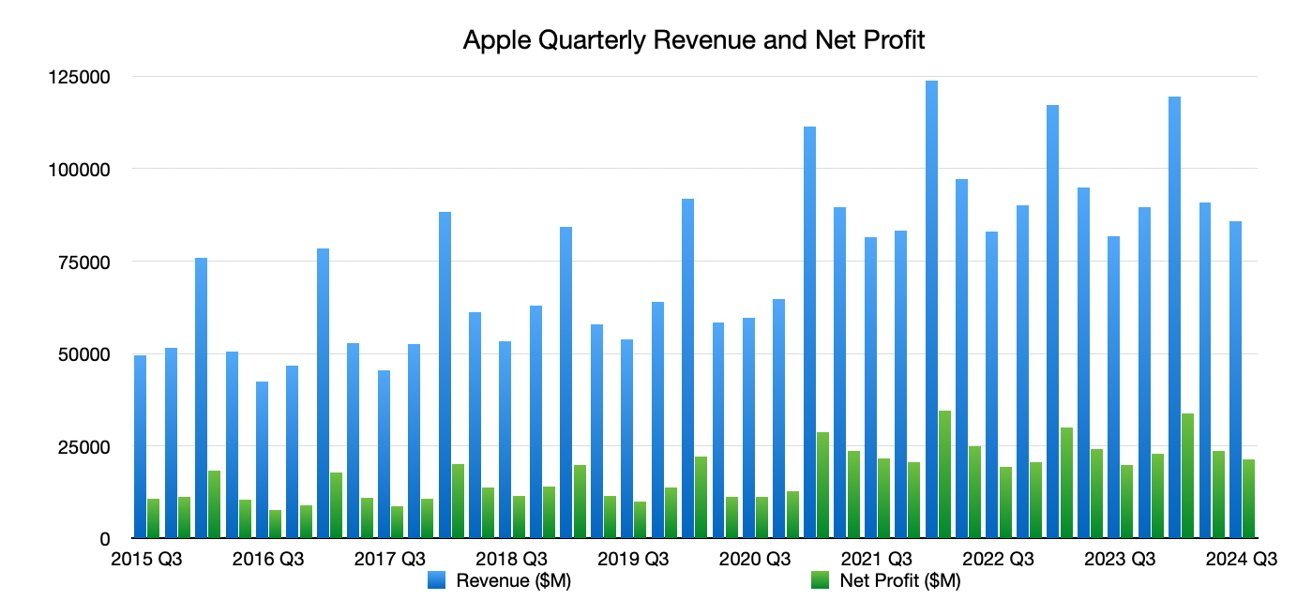

For Q4 2023, Apple reported overall revenue of $89.5 billion, down year-on-year by 0.7%. The earnings per share at the time was set at $1.46.

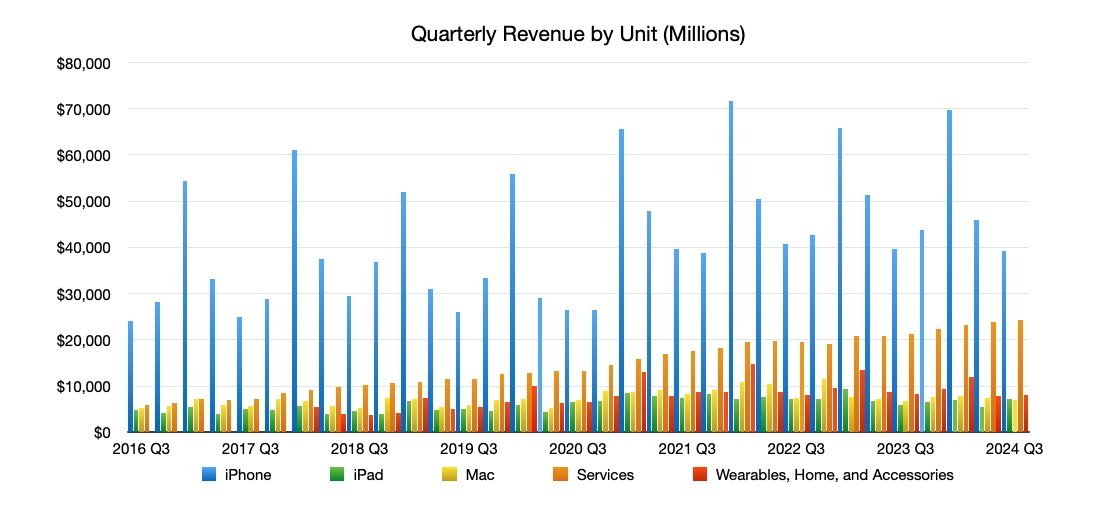

The important iPhone revenue went up 2.8% year-on-year to $43.8 billion. Services also saw continued growth of 16.3% to $22.3 billion.

By contrast, iPad's $6.4 billion revenue was a drop of 10.2% year-on-year. Mac revenue went down further, 33.8% year-on-year to $7.6 billion.

Wearables, Home, and Accessories dropped too, but at a lower 3.4% to $9.3 billion.

The Q3 2023 launches, including full-quarter sales of the M2 Max and M2 Ultra versions of the Mac Studio, a New Mac Pro with Apple Silicon, and a 15-inch MacBook Air should've helped the Q4 2023 results. There were also updates to the iPhone 15 generation, AirPods Pro with USB-C, USB-C Earpods, the Apple Watch Series 9, and the Apple Watch Ultra 2 toward the end of the quarter.

One quarter ago - Q3 2024

While not as useful for comparative purpose than Q4 2023, the Q3 2024 results are where the Q4 2024 results start off from.

The period saw revenue rise year-on-year to $85.78 billion, with an earnings per share of $1.40.

iPhone revenue was flat at $39.3 billion, down YoY by 0.9%. Wearables, Home, and Accessories also saw a drop of 2.3% to $8.01 billion.

Meanwhile, iPad jumped YoY by 23.7% to $55.6 billion, Mac raised 2.5% to $7.45 billion, and Services enjoyed 14.1% growth to $23.9 billion.

Full year - 2023

The results will also include full-year revenue for Apple, across all four quarters. Naturally, this can be compared to 2023's version.

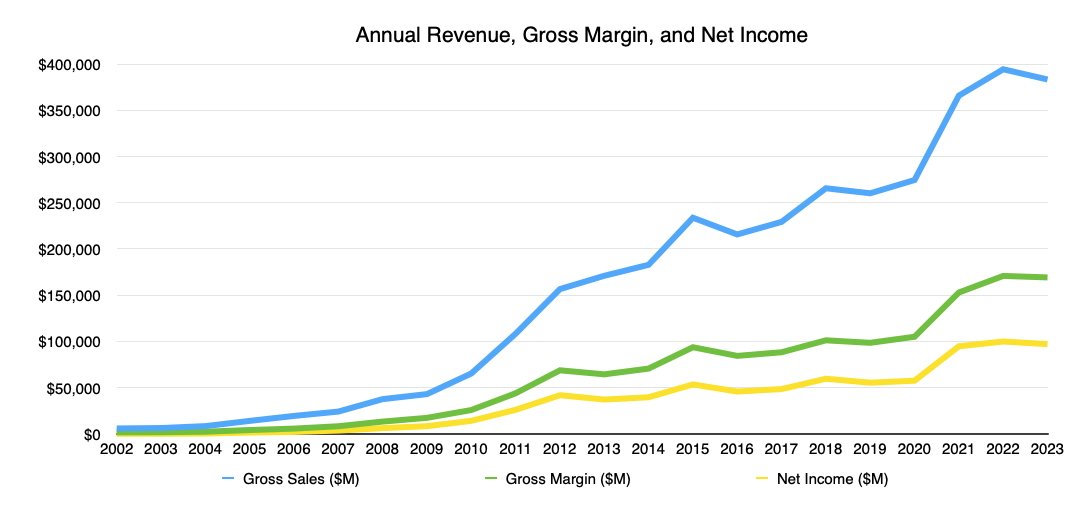

For 2023, the gross sales hit $383.3 billion, down 2.8% from 2022's record. Gross margin reached $169.1 billion, also down 1% against 2022.

For 2024 so far, Apple's gross sales are at $296.1 billion, with a gross margin of $136.8 billion. To beat the 2023 full-year result, Apple has to report at least $87.2 billion in revenue for Q4.

Wall Street Consensus

The Wall Street consensus refers to a survey of analysts. The results are averaged out to give a general opinion of where investors and analysts are leaning in their quarterly forecasts.

Yahoo Finance

In the estimates published by Yahoo Finance as of October 24, 26 analysts offered an average revenue estimate of $94.4 billion. The estimate's range goes from a high of $97.74 billion to a low of $93.75 billion.

For the earnings per share, a group of 27 forecasts an average of $1.55, with a high of $1.65 and a low of $0.92.

TipRanks

On October 23, TipRanks offered its own consensus figures. Based on 25 analysts, the revenue averages at 94.3 billion for the quarter, with a high of $98 billion and a low of $93 billion.

It adds that 20 out of the 25 analysts boosted revenue projections over the last three months. When it comes to EPS, 21 out of 26 analysts also raised estimates, also a sign of optimism.

The consensus for the earnings per share was averaged at $1.59, with a high of $1.65 and a low of $1.53.

Zacks

On October 24, Zacks' consensus estimate puts Apple at having revenue of $94.43 billion. This is up 5.5% year-on-year.

For the earnings per share, the consensus is $1.54 per share, again up 5.5% year-on-year. However, it adds that the estimate has been revised 0.9% lower over the course of 30 days.

Analysts

As time shortens before Apple actually issues its results, analysts at various financial institutions offer their own forecasts for Apple's quarter.

Morgan Stanley

On October 22, Morgan Stanley offered a forecast of a 2% revenue beat for Apple's upcoming results. For the EPS, Morgan Stanley thinks it will be a 4% beat, too.

The firm offered more focus about the December quarter, with the Q1 2025 results likely to be 1% down from consensus for revenue, and 2% down for EPS forecasts. It blames "mixed iPhone data points" that point to more constrained quarterly iPhone shipments.

However, it still feels that "any stock underperformance will be shortlived." Therefore it maintains an "Overweight" rating and a $273 price target.

Loop Capital

On October 22, Loop Capital reported a revision to its iPhone revenue forecast, with stronger-than-anticipated iPhone shipments. The supply chain is doing better than it previously forecasted, with signs of strong demand.

For iPhone revenue, Loop Capital upgraded its estimate from $48.6 billion to $49.3 billion.

It also maintains a buy rating on the shares, with a price target of $300.

Piper Sandler

In an October 28 note to investors, Piper Sandler proposed that the full-year revenue for Apple in 2024 will be $390.174 billion. The earnings per share for the entire year is anticipated to reach $6.69.

The analysts referred to earnings calls from major US carriers when discussing the iPhone 16, including how it is "down slightly over last year's levels on an introduction." T-Mobile commented that upgrade rates were low, thanks to consumers having more expensive and more durable devices on hand.

Data collected by the firm indicates "the iPhone 16 cycle isn't materially different from the most recent cycles," and that consumers are holding onto their devices for longer. Meanwhile, expectations that Apple Intelligence will help drive first-adopter updates are apparently unfounded.

J.P.Morgan

The October 28 note from J.P.Morgan anticipates a "better than expected" quarter, but with weaker than expected guidance for the following quarter. Shipment estimates for the iPhone 16 benefit from a smooth supply ramp, but sell-through for the iPhone 16 started slower than the iPhone 15.

Apple Intelligence helps improve shipment estimates avoid being downgraded, with 245 million units now expected to ship in 2025.

For the figures, J.P.Morgan raised its revenue and earnings forecast for the quarter to $95.9 billion and $1.63 respectively, versus its consensus of $94.2 billion and $1.59. Mac revenue will trend relative to Q3's results, while iPad will decelerate.

Services will, of course, remain consistent.

It has a price target for Apple's shares of $265.

TD Cowen

Apple will enjoy 6% better revenues year-on-year for the quarter, says TD Cowen, a percentage that will be matched by the following quarter.

The sell-in forecast for iPhone has grown from 46M to 48M units, with an 80M forecast for Q1 2025 maintained. Apple Intelligence's phased rollout could lead to "lower upgrade demand."

iPad and Mac have expectations of in-line demand based on seasonality, with favorable consecutive-quarter raises of about 20 to 25% expected for Apple Watch and AirPods.

Services will see continued growth by 14%, the note adds, though regulatory risks are a "modest headwind" due to European rule changes affecting payments and the App Store.

TD Cowen has a price target of $250 for AAPL.

Wedbush

Wedbush's October 27 note to investors discusses the rollout of Apple Intelligence, and will ultimately "kick off a true supercycle for Apple." Strong iPhone performance is expected for the September quarter, with a "relatively bullish" December demand commentary expected from the conference call.

That supercycle could be considerable, with approximately 300 million iPhones in the world that are four years old and ripe for upgrades. Apple could end up selling over 240 million iPhones in 2025, the analysts reckon, with 100 million Chinese iPhone upgrades possible as Apple Intelligence eventually rolls out to that region.

Wedbush has a price target of $300 for Apple, with an "Outperform" rating.

Evercore ISI

In Evercore's October 29 note, it points to a "more bearish" sentiment about Apple in recent weeks, with production cut noise lowering expectations for stock buyers.

For the results themselves, Apple is anticipated to deliver "in-line results" and that guidance and iPhone commentary will be "incrementally better vs fears." Risk in China is "overstated," and will be countered by developing market growth and a strong US upgrade cycle.

The Apple Intelligence rollout could also result in a "stronger for longer iPhone upgrade cycle."

Ultimately, Evercore forecasts Apple to outperform against low expectations. It maintains its "Outperform" rating and $250 price target.

AppleInsider will update this post when more analyst expectations become available.